Effective Strategies for Managing an Appraiser Shortage

4/8/2026

Is there an appraiser shortage? While most appraisers say “no", longer turn times and publicly available data suggest otherwise. Since the number of appraisers peaked in 2007, productivity improvements and generally stable loan demand have reduced the overall need. But a continued decline in the number of appraisers per Appraisal Subcommittee (ASC)[1] data suggests the industry is facing a potential shortage.

It takes years for new entrants to meet educational and experience requirements before they can independently perform assignments that comply with the Uniform Standards of Professional Appraisal Practice (USPAP). This long developmental period creates a lag in appraiser capacity to meet loan growth, especially when there is a surge in demand from new loans.

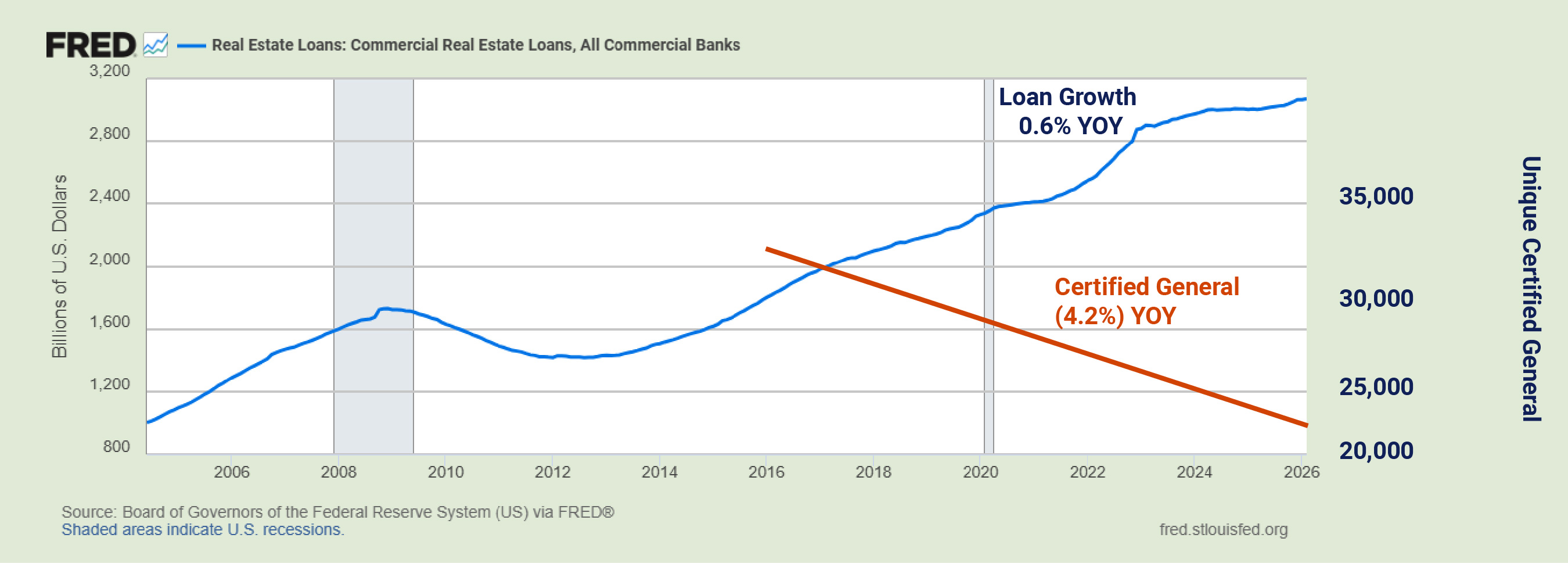

Data provided by the Board of Governors of the Federal Reserve System[2] shows commercial real estate loan volume in all commercial banks grew 0.6% year-over-year from 2020 through 2025 thanks to a combination of new construction, appreciation, and other factors. The number of certified general appraisers increased by just 0.1% during the same timeframe, ASC statistics show. However, this count is overstated as many certified general appraisers hold a credential in multiple states.

A more concerning trend emerges in the number of unique certified general appraisers, which has declined by more than 20% over the past five years (see graph).

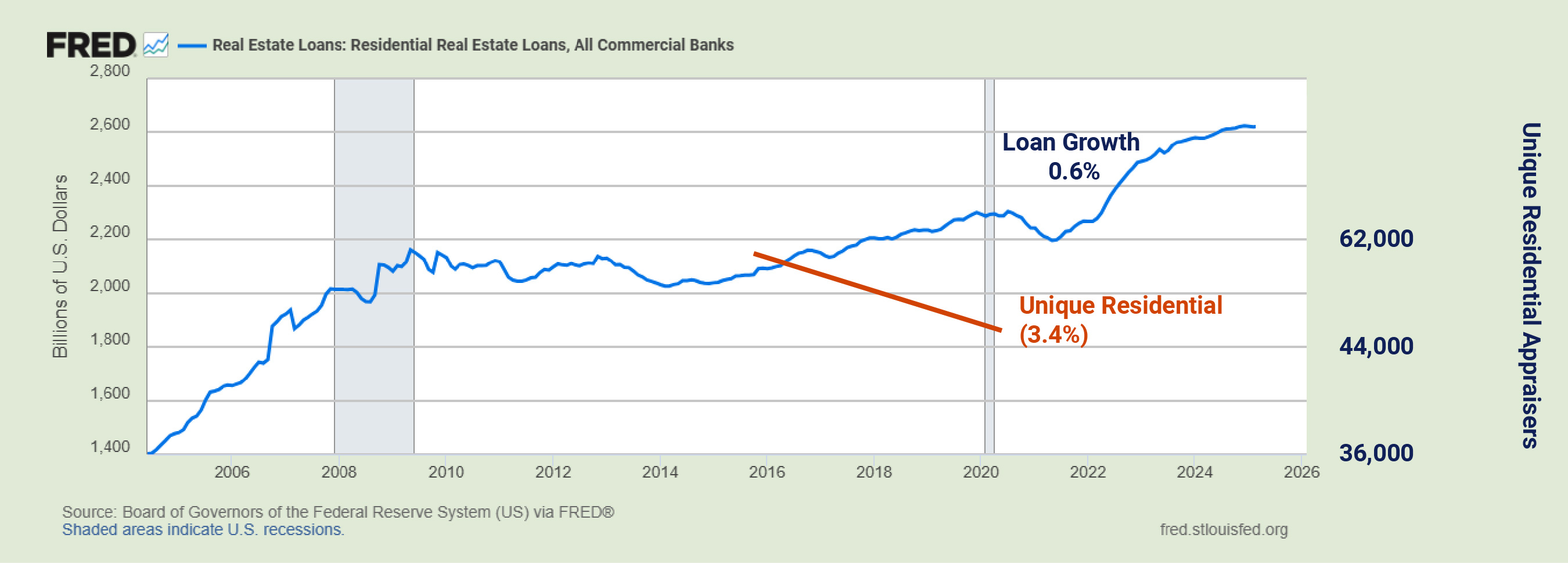

A similar concern appears when comparing residential loan volume to the number of unique residential appraisers.

A deeper dive into the ASC database as of year-end 2024 finds that 66,715 appraisers hold about 91,000 credentials[3] as compared with U.S. Bureau of Labor Statistics employment data[4] reporting 59,070 as. The difference may be due in part to appraisers who are not actively practicing. For example, one industry source[5] estimates that 15% of all residential appraisers currently provide appraisal-related services, such as managing the process or reviewing reports, but don’t produce appraisal reports. Overall, the data corroborates that there is a declining trend in the number of real property appraisers.

Effective strategies to ensure that lenders’ ability to process real estate-secured transactions in a timely manner is not impacted by a scarcity of appraisers include:

Use more carrots, less stick

- Pay appraisers well for delivering good quality appraisal reports that support the value conclusion while saving your organization money due to less staff time spent on “fixing” them.

- Engage appraisers for their such as for complex or atypical commercial, residential, or agricultural properties, as the valuation process can be more art than science at times, especially when little supporting information is available.

- Respect reasonable turn times rather than requesting rush appraisal deliveries when they are truly not needed to maintain report quality and reduce appraiser burnout.

Order alternative valuation products

- Use regulatory exceptions from the appraisal requirement and order alternative valuation products, such as evaluations or validations, to originate small-dollar loans and renew credit to existing borrowers, even if new funds push the loan amount over the regulatory dollar thresholds.

- Form strategic partnerships with third-party vendors who leverage technology to deliver compliant alternative valuation products in a cost-effective and efficient manner, instead of vendors who generate “low-cost, low-quality” products that may not comply with the regulations.

- Create mutually beneficial relationships where lenders receive conforming evaluations and validations in shorter turn times while borrowers obtain loans with lower closing costs.

Stop policing typos, start managing risk

- Set clear thresholds (Materiality Tests) within the review process for both residential and commercial transactions which allows reviewers to accept minor mistakes without having to contact the appraiser or vendor. This strategy enables all parties (reviewers, appraisers, and vendors) to focus their time on what really matters––errors that potentially raise legal concerns or materially impact the value conclusion. The Materiality Tests can provide parameters that address three primary types of significant concerns:

- Legal errors. Correct key factual mistakes in legal information, property characteristics, legal description, owner or borrower names, address, county, zoning, regulatory definitions, or appraiser certification.

- Bias or discrimination. Investigate allegations of appraiser bias or discrimination whether internal or external.

- Mistakes in value conclusion. Establish thresholds based on the value conclusion to determine when errors are or are not material. For example, some organizations set a “5% Rule” –– errors that impact the market value by 5% or less are accepted without requested revisions.

- Disregard minor issues. Typographical, grammatical, and stylistic preferences that do not meet the Materiality Test are inconsequential. Mention them in the appraisal scorecard if necessary, but they do not warrant further time or pursuit.

- Verify the accuracy of the property description and ensure all essential information is available at the onset of engaging the appraiser or vendor to minimize errors, reduce costs, and improve turnaround times.

Begin building your bench now

- Waiting to build your bench is like waiting for avocados to ripen. Oops! Too late! Start building your bench today so you will have appraisers available tomorrow.

- Seek competent appraisers as well as newer entrants to the industry for your approved vendor panel. Third-party vendor management should focus on quality, not quantity.

- Offer internships to potential new candidates who can train under a qualified supervisory appraiser.

Mind your manners, even when others do not

- Treat appraisers and vendors in a professional manner throughout the process to promote a collaborative rather than an adversarial relationship.

- Provide appraisers and vendors with a “scorecard” that rates both product (technical) and interaction (interpersonal) skills. This process will give them constructive feedback and assist lenders in deciding whether they should be engaged for future assignments.

- Recognize that the development of a value conclusion involves judgment, assumptions, and estimates. A market value that significantly differs from expectations may mean the lender needs to reassess the terms of the loan, not that the appraiser botched the assignment.

In summary, data shows the financial industry is facing a potential shortage of appraisers. Whether there will be enough appraisers to complete residential or commercial real estate assignments in a timely manner in the future remains to be seen. Lenders who implement effective strategies to allocate appraiser resources based on transaction risk, use compliant alternative valuation products when permitted, and apply materiality tests in their review processes can minimize the impact of appraiser shortages and stay competitive during periods of high loan demand.

By Beverlea Gardener

Beverlea S (Suzy) Gardner is an FDIC Appraiser (Retired)

[1] See at FFIEC Appraisal Subcommittee 2024 Annual Report.

[2] See at Real Estate Loans: Commercial Real Estate Loans, All Commercial Banks (CREACBM027NBOG) | FRED | St. Louis Fed.

[3] See at Analysis of 2025 ASC Appraisal License Data – Appraisal Buzz.

[4] See at Occupational Employment and Wage Statistics Profiles, Major Occupational Group is Business and Financial Operations and Detailed Occupations is Property Appraisers and Assessors.

[5] See at Residential Appraiser Trends Since 2016; New Projections for 2025-2030 - MtgeFi.